1168 お客様のコメント

1168 お客様のコメント

質問 1:

JJ's current share price is $1.80, with a dividend of $0.20 a share just about to be paid.

Dividends have increased at an average annual growth rate of 4.5% and this is expected to continue into the future.

What is JJ's cost of equity?

A. 16.1%

B. 12.5%

C. 11.1%

D. 17.6%

正解:D

質問 2:

XY has in issue a 6% convertible bond which is redeemable at par or convertible into equity shares in one year's time. The conversion terms are 20 equity shares for each $100 of convertible bond. The conversion value in one year's time is expected to be $105 per $100 nominal of the bond based on the current share price of $5.25.

Which of the following statements about the bond is correct?

A. The bond will be converted into equity shares in one year's time if the share price does not change.

B. If the bond is redeemed rather than converted that means that the investor will receive $105 for each

$100 of nominal value.

C. The yield to maturity of the convertible bond is a constant 6%.

D. XY's post tax cost of debt for the convertible bond will be higher than the yield to maturity.

正解:A

質問 3:

YZ issued $100,000 6% convertible bonds at par on 1 January 20X5. The bondholders have the option to convert into equity shares in 3 years' time or redeem at par for cash on the same date.

Interest is paid annually in arrears and bonds issued by similar entities without conversion rights pay interest at 8%.

What is the value of equity to be recognised in YZ's statement of financial position as at 31 December

20X5?

Give your answer to the nearest whole $.

$?

正解:

5138

質問 4:

RS has issued an instrument with a nominal value of $1 million, at a discount of 2.5%, and a coupon rate of 6%. The terms of the issue are that the instrument must either be redeemed at par, at the option of the holder, in three years' time, or alternatively converted into equity shares in RS.

The characteristics of this instrument taken as a whole indicates that it would be classifed as which of the following?

A. Equity instrument

B. Debt instrument

C. Compound instrument

D. Discounted instrument

正解:C

質問 5:

Which of the following statements are incorrect regarding identifiable assets? Select ALL that apply.

A. Contingent assets and liabilities are examples of exceptions to the rules governing identifiable assets

B. To be identifiable assets must be separable from the subsidiary

C. Net assets must be identifiable at acquisition

D. Deferred tax assets and liabilities are not classed as identifiable assets

E. Assets can also be identifiable if they arise from contractual or legal rights

正解:A,D

質問 6:

An entity has declared a dividend of $0.12 a share. The cum dividend market price of one equity share is

$1.40.

Assuming a dividend growth rate of 7% a year, what is the entity's cost of equity?

A. 17.0%

B. 8.6%

C. 16.2%

D. 9.4%

正解:A

質問 7:

The following is extracted from MN's statement of financial position at 30 September 20X1.

Calculate the gearing (measured as debt:equity) ratio of MN at 30 September 20X1.

Give your answer to one decimal place.

%

正解:

63.8, 63.78, 63.7, 63.80

質問 8:

At 31 October 20X1 RS has in issue 10% debentures 20X8 with a carrying value of $350,000.

Extracts from its statement of profit or loss for the year ending 31 October 20X7 are as follows:

What is the interest cover for RS for the ended 31 October 20X7?

A. 11.1 times

B. 10.0 times

C. 8.0 times

D. 9.0 times

正解:D

質問 9:

On 1 January 20X4 EF grants each of its 125 employees 500 share options on the condition that they remain in employment for 3 years. During the year to 31 December 20X4 10 employees left and It is expected that a further 25 will leave before the end of the vesting period.

The fair value of each share option is $30 on 1 January 20X4 and $45 on 31 December 20X4.

What is the journal entry in respect of these share options in EF's financial statements for the year ended 31 December 20X4?

A. Option C

B. Option A

C. Option D

D. Option B

正解:B

JJ's current share price is $1.80, with a dividend of $0.20 a share just about to be paid.

Dividends have increased at an average annual growth rate of 4.5% and this is expected to continue into the future.

What is JJ's cost of equity?

A. 16.1%

B. 12.5%

C. 11.1%

D. 17.6%

正解:D

質問 2:

XY has in issue a 6% convertible bond which is redeemable at par or convertible into equity shares in one year's time. The conversion terms are 20 equity shares for each $100 of convertible bond. The conversion value in one year's time is expected to be $105 per $100 nominal of the bond based on the current share price of $5.25.

Which of the following statements about the bond is correct?

A. The bond will be converted into equity shares in one year's time if the share price does not change.

B. If the bond is redeemed rather than converted that means that the investor will receive $105 for each

$100 of nominal value.

C. The yield to maturity of the convertible bond is a constant 6%.

D. XY's post tax cost of debt for the convertible bond will be higher than the yield to maturity.

正解:A

質問 3:

YZ issued $100,000 6% convertible bonds at par on 1 January 20X5. The bondholders have the option to convert into equity shares in 3 years' time or redeem at par for cash on the same date.

Interest is paid annually in arrears and bonds issued by similar entities without conversion rights pay interest at 8%.

What is the value of equity to be recognised in YZ's statement of financial position as at 31 December

20X5?

Give your answer to the nearest whole $.

$?

正解:

5138

質問 4:

RS has issued an instrument with a nominal value of $1 million, at a discount of 2.5%, and a coupon rate of 6%. The terms of the issue are that the instrument must either be redeemed at par, at the option of the holder, in three years' time, or alternatively converted into equity shares in RS.

The characteristics of this instrument taken as a whole indicates that it would be classifed as which of the following?

A. Equity instrument

B. Debt instrument

C. Compound instrument

D. Discounted instrument

正解:C

質問 5:

Which of the following statements are incorrect regarding identifiable assets? Select ALL that apply.

A. Contingent assets and liabilities are examples of exceptions to the rules governing identifiable assets

B. To be identifiable assets must be separable from the subsidiary

C. Net assets must be identifiable at acquisition

D. Deferred tax assets and liabilities are not classed as identifiable assets

E. Assets can also be identifiable if they arise from contractual or legal rights

正解:A,D

質問 6:

An entity has declared a dividend of $0.12 a share. The cum dividend market price of one equity share is

$1.40.

Assuming a dividend growth rate of 7% a year, what is the entity's cost of equity?

A. 17.0%

B. 8.6%

C. 16.2%

D. 9.4%

正解:A

質問 7:

The following is extracted from MN's statement of financial position at 30 September 20X1.

Calculate the gearing (measured as debt:equity) ratio of MN at 30 September 20X1.

Give your answer to one decimal place.

%

正解:

63.8, 63.78, 63.7, 63.80

質問 8:

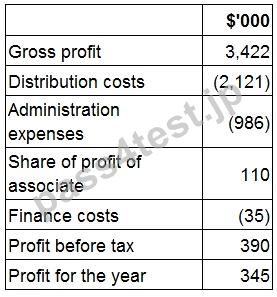

At 31 October 20X1 RS has in issue 10% debentures 20X8 with a carrying value of $350,000.

Extracts from its statement of profit or loss for the year ending 31 October 20X7 are as follows:

What is the interest cover for RS for the ended 31 October 20X7?

A. 11.1 times

B. 10.0 times

C. 8.0 times

D. 9.0 times

正解:D

質問 9:

On 1 January 20X4 EF grants each of its 125 employees 500 share options on the condition that they remain in employment for 3 years. During the year to 31 December 20X4 10 employees left and It is expected that a further 25 will leave before the end of the vesting period.

The fair value of each share option is $30 on 1 January 20X4 and $45 on 31 December 20X4.

What is the journal entry in respect of these share options in EF's financial statements for the year ended 31 December 20X4?

A. Option C

B. Option A

C. Option D

D. Option B

正解:B

Jinbo -

F2独学等の良い相棒になってくれると思います。これだけ内容が充実しているのにこの安さは正直驚きです。